Products

Resources

Company

October 3, 2019

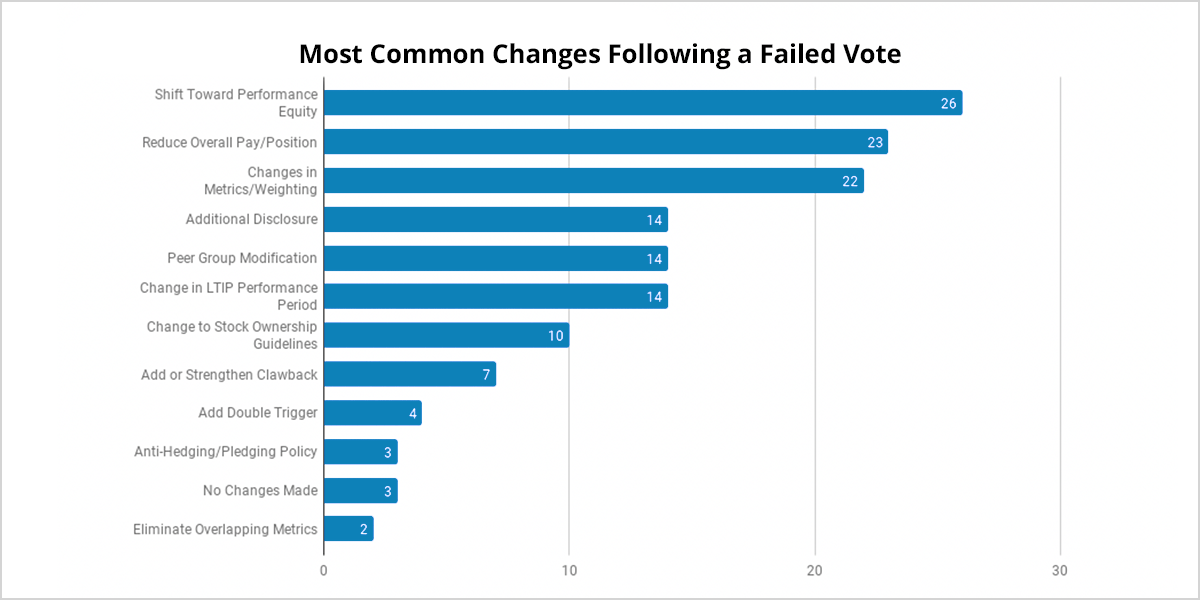

Eight years following the introduction of Say on Pay in 2011, shareholder voices are more pronounced than ever when it comes to executive compensation. In 2018, 49 Russell 3000 companies failed their Say on Pay votes. Say on Pay may be a non-binding, advisory vote, but failure reflects shareholder dissatisfaction with executive pay or company performance. Therefore, it is in the company’s best interest to seek feedback from its investors in order to make changes that will secure affirmative votes in the following year. This Equilar study examined how companies disclosed their responses in their proxies in the year following a failed Say on Pay vote. It appears that Say on Pay remains effective in incentivizing companies to disclose evident changes to their compensation plans. The principal finding is that these changes do have a direct effect on shareholder voting behavior. Companies that failed Say on Pay in 2018 most frequently stated their intent to increase the proportion of long-term incentive plan grants strictly tied to performance. The second- and third-most commonly disclosed changes were a reduction in overall pay and changes in metrics or weighting, respectively.

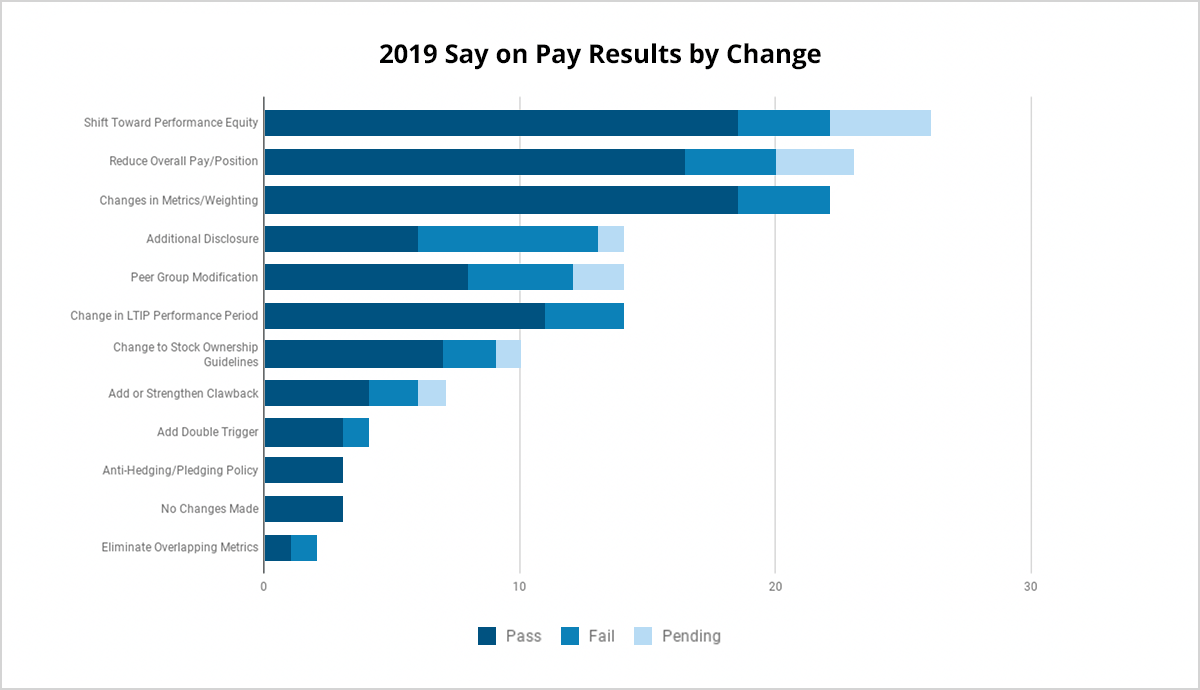

The chart below demonstrates the frequency of the most common changes disclosed following failed 2018 Say on Pay votes:

Just over half of the companies that failed Say on Pay in 2018 elected to make changes embodying a shift toward performance equity. This shift resulted, most frequently, in a pay mix leaning heavily on variable pay. This could take multiple forms: the introduction of a new equity plan emphasizing performance grants, tying equity previously granted as one-time awards to an annual financial metric, or the reduction of time-based equity. Cleveland Cliffs, which saw a jump from 32.6% to 70.6%, chose to “increase the portion of the annual incentive program based on a financial performance metric.” Similarly, Qualys increased the portion of its CEO compensation tied to performance to 54%, and eliminated “catch-up” restricted stock unit grants, disclosing all these changes in a graph. A reduction in overall pay was marked by the removal of unique or one-time incentives, without noting a shift to performance-based equity. Disclosure indicating that executives’ base salaries or bonuses were held constant was also categorized as a reduction in overall pay. Compensation metric changes for 2019 generally consisted of modifiers or the addition of line-of-sight metrics to long-term incentive plans. iStar, for example, established a metric that would cap funding at the threshold level for the Annual Incentive Plan if total shareholder return is negative.

Bed Bath & Beyond attracted significant attention in the last year with its Say on Pay results after another year of poor company performance. Following the vote in 2017, which only received 43.9% approval, the company only made one change to its compensation plan—the reduction of overall pay for its former CEO, Steven Temares. For 2018, Bed Bath & Beyond reduced CEO target compensation by 19%, which involved a $2.2 million decrease in the value of equity awards as well as the voluntary waiver of $500,000 of the Temares’ annual base salary. However, these actions did little to appease shareholders and the 2018 plan garnered even less support, with only 21.4% of votes in favor. Bed Bath & Beyond serves as an example of how simply paying executives less will not suffice—shareholders want to see clear compensation plans that will result in visibly improved company performance. It remains to be seen whether changes affected in 2019, including further reductions in CEO equity compensation, will result in an improvement in Say on Pay approval percentage.

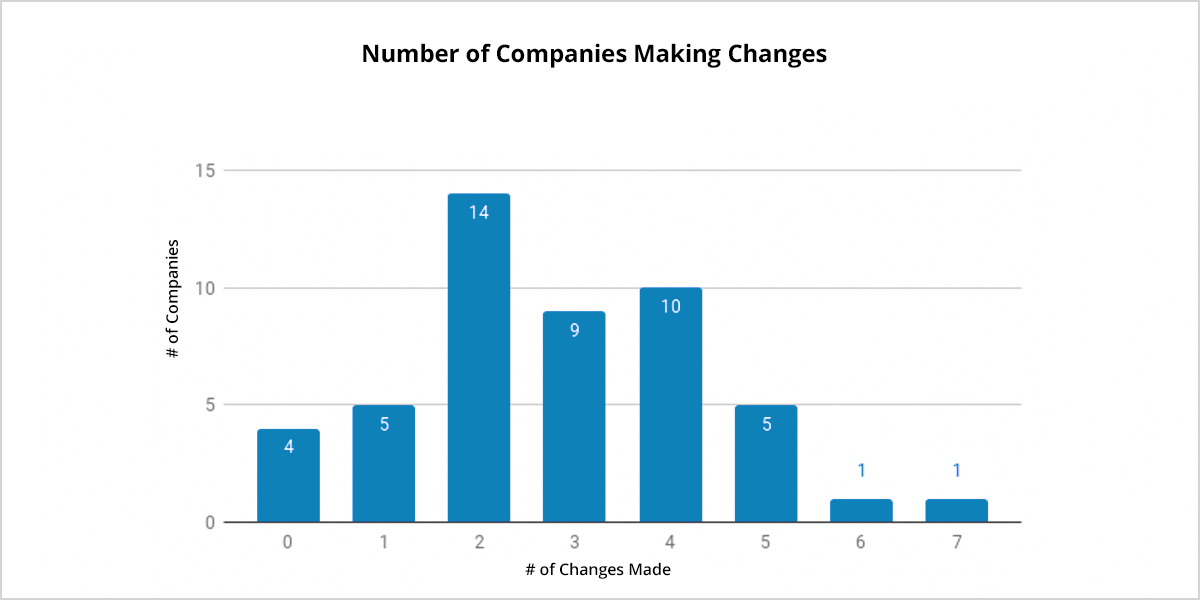

While the vast majority of Russell 3000 companies with failed Say on Pay votes in 2018 made changes to their executive compensation plans for 2019, the number of changes made varies. 81.6% of companies made at least two changes. Companies most frequently implemented two changes, with 28.6% of companies choosing to do so. Qualys, Inc. made seven modifications in response to its failed vote, the highest number among the Russell 3000, and saw a dramatic jump in its Say on Pay approval from 38.8% to 97.3%. Only three companies failed to disclose any changes specific to Say on Pay failure. Interestingly enough, all three of these companies went on to pass their 2019 votes. Shareholder approval on executive compensation at one of these companies, Trinseo S.A., actually went from 44% in 2018 to 94% in 2019, despite a 42.8% decline in stock price and the implementation of a stock repurchase program. The other two companies passed by much smaller margins. Cogent Communications, for example achieved 58% approval.

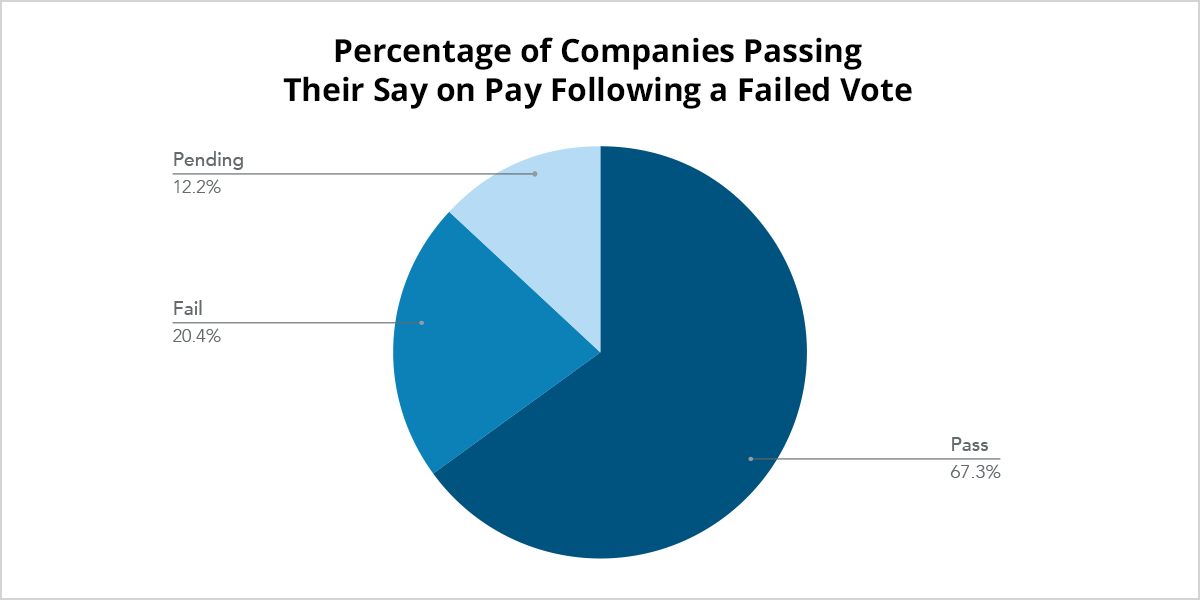

It is worth investigating whether or not these amendments have been enough to placate shareholder concerns. Most companies that failed Say on Pay in 2018 have already held their 2019 votes. 67.3% of Russell 3000 companies with failed 2018 votes have passed their 2019 votes so far, and 20.4% have failed. The results of 12.2% of the companies are still pending. Of the companies who have held their 2019 votes so far, Wynn Resorts, Limited has seen the greatest improvement in its Say on Pay approval, with a 76.3 percentage point increase. Wynn Resorts disclosed four changes in response to shareholder concerns. These changes included the three most common actions—a shift toward performance equity, the reduction of overall pay or position and changes in metrics or weighting—as well as a change in the long-term incentive plan performance period. The company also experienced a leadership transition that may have impacted shareholder opinion and, consequently, board actions, as the former CEO and founder, Steve Wynn, stepped down in early 2018 amid sexual-misconduct allegations. While the complete 2019 voting results have yet to be seen, the changes do seem to have had some positive impact on compensation package approval.

A deeper dive into these companies shows the effectiveness of the broad range of changes made. As demonstrated by the graph above, companies that implemented changes involving metrics and favoring performance equity passed 2019 Say on Pay votes in the highest proportion. Companies that provided for the overall reduction of pay also garnered support. Although the sample size of companies that provided an additional compensation disclosure is limited, from the results seen thus far, this particular change has not in itself proved very effective.

Based on these findings, it might be inferred that shareholders of these companies are primarily concerned with the clear evidence of changes to executive compensation plans. Furthermore, issuers and their compensation and benchmarking teams appear to be catching on to this, as they affect changes that directly impact pay. While this appears to be done primarily through a shift to performance equity, there are two other, primary avenues for doing this as well: metric changes or a visible reduction in pay. With increasing frequency, these changes are clearly disclosed and highlighted in organized charts and tables, a testament to clarity over convolution in CD&As.

Perhaps this bolsters the case for Say on Pay’s legislative success: a direct reduction in pay is the most visible means for earning shareholder approval. In other words, Say on Pay appears to be incentivizing the behavior it was intended to incentivize. That being said, considering only a small portion of companies fail their Say on Pay votes to begin with, this does not mean that giving shareholders an advisory vote on compensation matters will directly result in the reduction of executive pay across the board.

As exemplified by Bed Bath & Beyond, shareholders prioritize company performance. During a good year, shareholders may likely not be concerned with executive compensation plans at all, regardless of their magnitude. For those companies that are not performing well, there is increased interest in the metrics that compensation committees use to determine compensation and how these measures relate to performance.

Methodology:

Failed Say on Pay votes are defined as those that achieved less than 50% shareholder approval.

Abstained votes are excluded from this calculation. The calculation used for Say on Pay voting is:

Say on Pay votes occurring in 2018 are defined by companies that held their annual general meetings between July 1, 2017 and June 30, 2018.

2019 votes are defined by companies with annual general meetings held between July 1, 2018 and June 30, 2019.

Erin Lehr, Research Analyst at Equilar, authored this post. Please contact Amit Batish, Content Manager, at abatish@equilar.com for more information on Equilar research and data analysis.

Subscribe to our Newsletter to stay informed about upcoming events and webinars.

If you'd like, we can send our newsletters straight to your inbox.