Products

Resources

Company

Our database is continually updated with the latest SEC filings to ensure timely information is captured.

We perform a thorough screening of our database through three rounds of quality and accuracy checks.

SureSource SEC EDGAR Technology allows users to drill down directly into the source document.

Equilar and The Center on Executive Compensation have partnered to develop the Incentive Plan Analytics Calculator (IPACSM). Assess the robustness of metrics used in your incentive plans.

See how enhancements to IPAC allow you to precisely analyze how your peers design individual incentive plans using payouts and weightings data.

Stay ahead of recent incentive plan changes among

your peer companies.

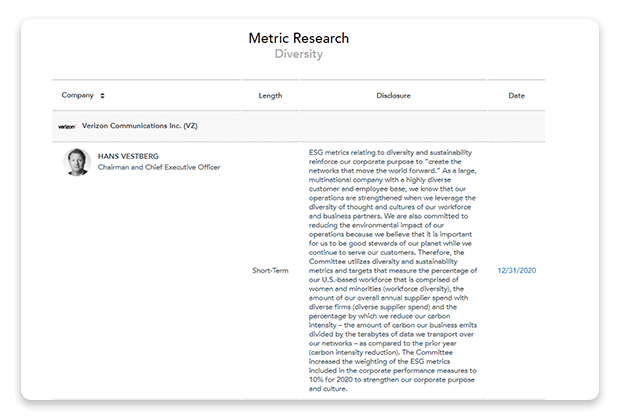

Assess metric usage and disclosures for diversity, ESG and all other metrics on an individual executive level.

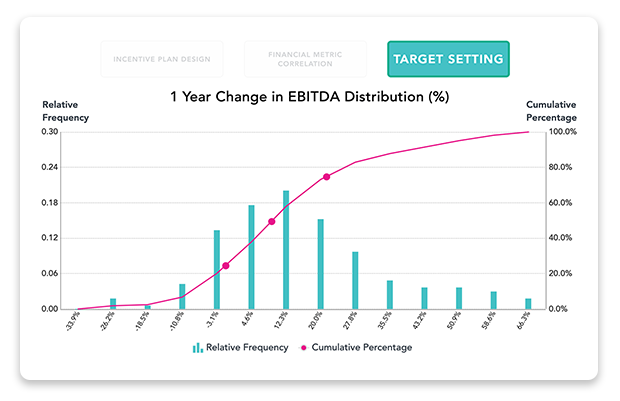

Choose from over 150 financial metrics to determine the statistical relationship to TSR over any time horizon.

Select targets based on historical performance of nearly

100 metrics and current market conditions.

Learn how professionals use IPAC to optimize and perfect

their incentive plans.

Share the challenges facing your team, and our data experts will present a custom solution to meet your specific needs.