Featured Content

Compensation & Governance Insights

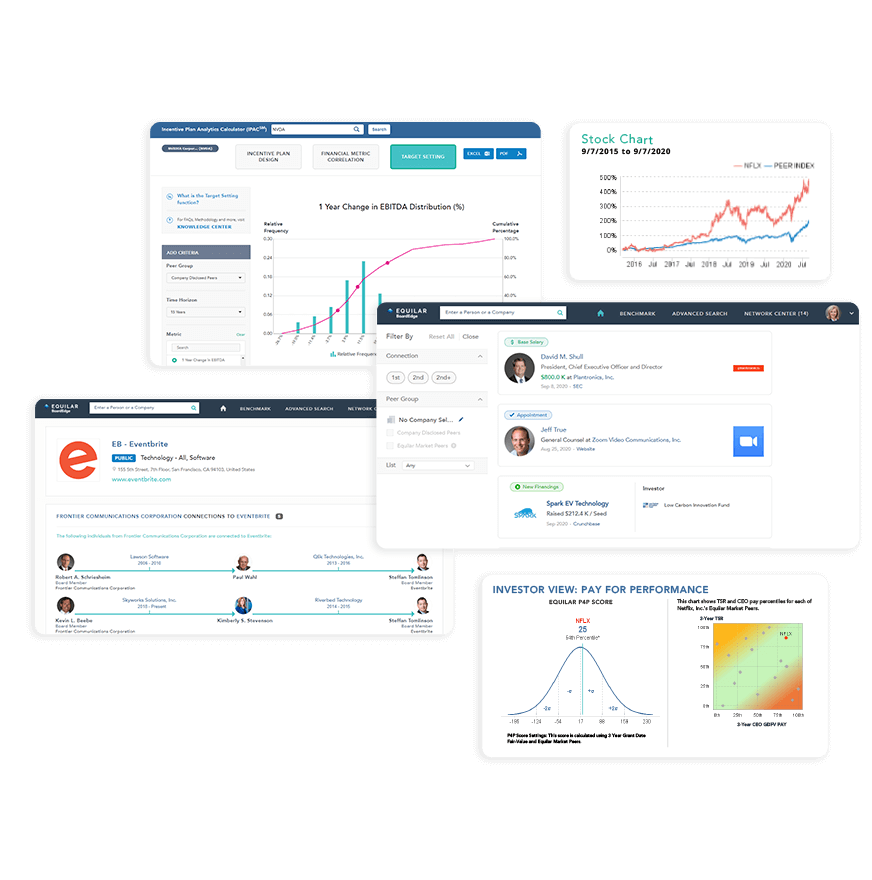

Board meeting preparation and analysis

Executive Compensation

Benchmark executive pay

ERIC (AI-Powered Proxy Analysis)

Extract proxy insights using AI

Visit the new ExecAtlas.com to learn more about ExecAtlas, our Executive Engagement and Relationship Intelligence platform.

Visit the new ExecAtlas.com to learn more about ExecAtlas, our Executive Engagement and Relationship Intelligence platform.

Products

Resources

|

|

|

|

Share the challenges facing your team, and our data experts will present a custom solution to meet your specific needs.

Stay up to date on the latest insights, trends and reports.

Solutions

These cookies are essential for moving around the website and using its features. Convenience features such as your login status and browser based optimizations all ensure performance and a good basic experience.

These cookies allow the website to remember the choices you make to provide personalized features. They are anonymous and do not track across different websites.

These cookies will monitor website performance and data about how visitors use our website. They help us understand how to improve our service and to determine where improvements can be made.